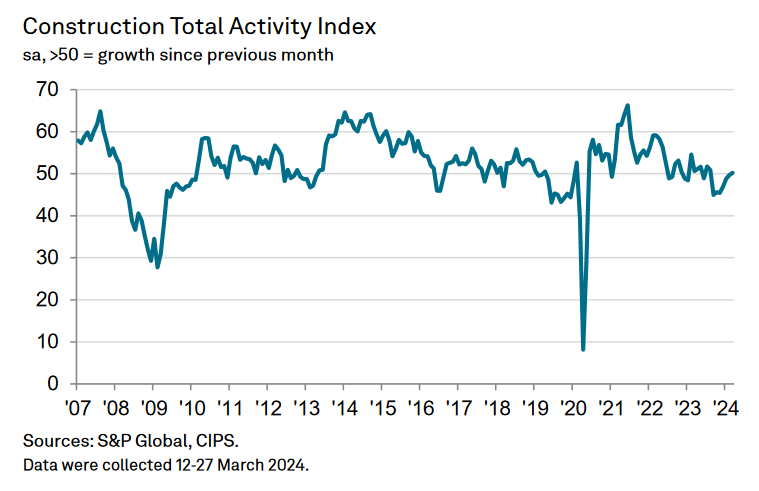

Construction sector returns to growth in March

UK construction companies indicated a renewed increase in total industry activity during March, thereby ending a six-month period of decline.

Respondents to the S&P Global UK Construction Purchasing Managers’ Index (PMI) survey often commented on a turnaround in sales pipelines and greater new business enquiries linked to the improving economic outlook and more stable financial conditions.

Adding to signs of a recovery in construction sector performance, new orders expanded at the fastest pace since May 2023. However, construction companies remained cautious about staff hiring, with employment numbers falling for the third month running in March.

The headline PMI rose from 49.7 in February to 50.2 in March. Any reading above 50.0 indicates an overall expansion of construction output. Although signalling only a fractional rise in business activity, the index was at its highest level since August 2023.

Civil engineering was the best-performing segment in March, as output levels increased at a marginal pace. Panel members cited increased work on infrastructure projects and resilient demand in the energy sector.

House building and commercial construction activity were both broadly unchanged in March. The stabilisation in residential work represented the best performance for this category since November 2022.

March data pointed to a moderate increase in new work received by construction companies. The rate of expansion accelerated since February and was the strongest for ten months. Anecdotal evidence pointed to a general rise in new project starts and greater tender opportunities across the construction sector so far in 2024.

In contrast to the positive trends for output and new orders, latest data signalled another reduction in staffing numbers. That said, the rate of job shedding was only marginal and eased since the previous month. At the same time, sub-contractor usage was stable in March. The latest survey indicated a strong improvement in sub-contractor availability. Rates charged by sub-contractors increased at the fastest pace since August 2023.

Purchasing costs rose for the third month running in March. However, the rate of inflation was only marginal and the weakest seen over this period. Survey respondents noted increasing transport costs, but others suggested that strong competition among suppliers had constrained the overall rate of input price inflation.

Suppliers’ delivery times shortened for the thirteenth consecutive month in March, albeit to only a moderate extent. Anecdotal evidence suggested that improving materials availability and subdued demand had contributed to improving vendor performance.

Construction companies remain upbeat about their prospects for business activity in the next 12 months. Around 49% of the survey panel anticipate a rise in output levels, while only 11% predict a decline. That said, the degree of optimism eased since February and was the lowest in 2024 to date. Survey respondents typically commented on stronger order books and hopes that broader market conditions will continue to improve, especially in relation to house building projects. Meanwhile, political uncertainty, squeezed margins and financial pressures were cited as factors weighing on optimism.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said: “UK construction output returned to growth in March as a renewed expansion of civil engineering work was supported by more stable conditions in the housing and commercial building segments. The marginal overall rise in total construction activity ended a six-month period of contraction.

“The near-term outlook for construction workloads appears increasingly favourable as order books improved again in March and to the greatest extent for just under one year. Construction companies generally commented on a broad-based rebound in tender opportunities, helped by easing borrowing costs and signs that UK economic conditions have started to recover in the first quarter of 2024.

“Staff hiring was a weak spot for the construction sector in March amid lingering concerns about margin pressures and continued risk aversion among major clients. Construction firms often reported delays with replacing departing staff, which led to a decrease in total employment numbers for the third month in a row.

“Supply chain pressures eased across the construction sector as subdued purchasing activity helped to alleviate strains on capacity. Improved supply conditions also led to a slowdown in the rate of cost inflation, which slipped to a three-month low in March.”

Brian Smith, head of cost management at AECOM, said: “The construction industry’s slump has thankfully stopped short of the seven-month mark, in time for more favourable weather conditions and with some of the financial pressures it has faced in recent times easing.

“With inflation continuing to fall, the Bank of England has opened the door to rate cuts anticipated in the next few months, easing finance costs which will boost the willingness of developers to push forward with paused projects.

“There remain challenges for construction firms in the short term. An increasingly competitive tendering market is expected to remain for rest of this year and, although some input costs are falling, labour shortages and the resulting price rises are challenges that will remain.”

James Bailey, director and housing leader at PwC UK, added: “March’s PMI data indicates a positive market reaction to the improving economic landscape and the subsequent financial stability being provided to both businesses and consumers, with the sector posting 50.2 - a display of slight growth.

“With housing and residential work, the PMI noted the category saw its best result since November 2022, with respondents referencing stronger order books amid optimism that broader market conditions will continue to improve, which will be crucial to boosting the availability and affordability of housing for consumers, as well as giving developers the right signals to continue with building plans and site activity.

“A key part of that momentum will be any new government establishing policies that enable and catalyse longer term supply. Planning has long been identified as a key constraint, a view which was shared by the CMA in its recent housebuilding market study. Additionally, industry players are increasingly cautious about the financial capacity of Housing Associations to meet Section 106 obligations, particularly given the need to channel significant investment into existing activity.

“Any shortfall in new build development activity here has the potential to constrain private supply. A combination of new long-term rent settlement, new grant funding and a reallocation of existing under-utilised grant funding will support existing players and help to attract more private capital into the affordable housing market. We expect more partnerships between housebuilders and private investors to be a trend going forward.”

Martin Beck, chief economic advisor to the EY ITEM Club, said: “March’s construction PMI showed the sector ending a six-month period of decline last month. An index of 50.2 was up from 49.7 in February and the first reading in expansionary, plus-50 territory since August 2023. Survey respondents cited lower borrowing costs and signs of a recovery in the wider economy as factors boosting construction activity. The fact that new orders rose at the fastest pace since last May bodes well for a further rise in the PMI over the next few months.

“Alongside evidence from the services and manufacturing PMIs of expansion in the economy’s other major sectors in March, the latest construction index adds to signs that the economy returned to growth in Q1 2024, following the mild technical recession in the second half of last year. The impact of public sector strikes will cap how much GDP grew in the first quarter, but the EY ITEM Club thinks a combination of lower inflation, rising real incomes and actual and prospective cuts in taxes and interest rates should see momentum in the economy continue to build this year.

“There was also better news in March’s S&P Global survey on cost pressures facing construction firms. The survey’s measure of input prices rose at the slowest pace in three months. With March’s services survey also indicating an easing in price pressures, the latest evidence is consistent with the expectation that inflation will fall significantly in the coming months and that the Bank of England should begin to cut interest rates soon.”