Housebuilding slump weighs on construction output

UK construction companies have indicated a decline in business activity for the third consecutive month during November, led by another sharp fall in residential building.

Elevated borrowing costs and subdued demand for new housing projects were widely cited as factors holding back construction activity.

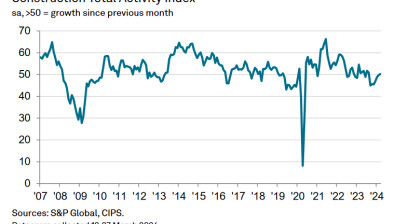

Latest survey data pointed to the steepest reduction in purchasing costs across the construction sector for more than 14 years. This was linked to lower raw material prices, alongside greater competition among suppliers in response to falling demand for construction inputs. The headline S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) – a seasonally adjusted index tracking changes in total industry activity – registered 45.5 in November, down fractionally from 45.6 in October and below the 50.0 no-change value for the third month running.

The latest reading was the second-lowest since May 2020 and signalled a marked reduction in total industry activity.

November data illustrated that house building (index at 39.2) remained by far the weakest-performing segment, followed by civil engineering (43.5). Survey respondents cited cutbacks to residential development projects and a general slowdown in activity due to unfavourable market conditions.

Commercial building showed some resilience (index at 48.1), but activity in this category has now decreased for three months in a row. Construction firms noted that lacklustre domestic economic conditions and delayed decision-making by clients on major investment spending had been factors limiting demand.

November data suggested a continued lack of new work to replace completed projects. Total new orders decreased for the fourth month running, albeit at the slowest pace since August. Customer hesitancy and greater borrowing costs were often reported as weighing on sales volumes, especially in the housing category.

Business activity expectations for the year ahead picked up from October’s recent low, but remained notably weaker than seen in the first half of 2023. Concerns about the near-term demand outlook contributed to a renewed decline in staffing numbers during November and a marked reduction in purchasing activity.

Input buying has now decreased in five of the past six months, largely reflecting reduced workloads and a lack of new project starts. Some firms also commented on destocking efforts in response to improved supply conditions, which led to lower input buying in November.

Average lead times among vendors shortened for the ninth successive month in November. That said, the rate of improvement has eased considerably since the summer. Survey respondents reported spare capacity among suppliers and weaker demand for construction inputs, although some commented on transportation delays.

A combination of greater price competition among suppliers and falling raw material costs contributed to another decrease in input prices across the construction sector. The overall rate of decline was the steepest since July 2009, with survey respondents reporting falling prices paid for a range of materials (especially steel and timber).

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said: “A slump in house building has cast a long shadow over the UK construction sector and there were signs of weakness spreading to civil engineering and commercial work during November. Residential construction activity has now decreased in each of the past 12 months and the latest reduction was still among the fastest seen since the global financial crisis in 2009.

“Elevated mortgage costs and unfavourable market conditions were widely cited as leading to cutbacks on house building projects. Rising interest rates and the uncertain UK economic outlook also hit commercial construction in November, while a lack of new work contributed to the fastest decline in civil engineering activity since July 2022.

“Improving supply conditions were evident again in November, linked to rising raw material availability and spare capacity across the supply chain. Greater competition among suppliers added to downward pressure on prices paid for construction products and materials. The latest survey indicated that overall input prices decreased for the second month running and at the fastest rate since July 2009.”

Dr John Glen, chief economist at the Chartered Institute of Procurement & Supply (CIPS), said: “There is no doubt that 2023 has been a difficult year for the UK construction sector. Inflated borrowing costs and falling demand have conspired to further slow new building this month.

“Despite this, the sector has finally emerged from a period of intense supply chain pressure and prices are now falling across the board, especially for timber and steel. Projects are no longer being delayed due to unexpectedly high material costs with November seeing the sharpest reduction in purchasing prices since July 2009.

“There will be no quick fixes next year for the sector. Lower demand, elevated interest rates and the prospect of an election promise an uncertain start to 2024. This is a challenging moment for suppliers in the sector, who may have tough price negotiations ahead.”

The Federation of Master Builders (FMB) said the continuing fall in construction output, accelerated by the decline in house building, demonstrates the sorry state of the economy, and the need for government measures to turbocharge economic growth.

Brian Berry, chief executive of the FMB, said: “Today’s S&P Global/CIPS UK Construction PMI figures mark a full year of continued decline in house building rates in Britain. The civil engineering and commercial sectors are now beginning to show weakness, and with employment rates also decreasing for the first time in ten months, there are worrying signs for the future of the construction industry. If we do not see significant government intervention to substantially boost the UK’s house building rates and ensure that people have access to the high-quality homes they require, this decline is likely to continue.

“The positive measures announced in last month’s Autumn Statement, such as the proposals to speed up planning decisions, and to provide tax cuts to small businesses, indicate an acknowledgment from the Government that action is needed. But these proposals alone do not go anywhere near far enough. A wide-reaching, industry specific plan will be necessary to support local house builders to ensure that they can deliver the scale of housing that Britain is currently in desperate need of.”

Brian Smith, head of cost management and commercial at AECOM, said: “The sector’s downturn continues for a fourth month running, with the current cold snap reminding us that we’re heading into the toughest part of the year for building.

“Firms will have been looking to the recent Autumn Statement for measures to stoke the sector’s fires and drive infrastructure investment. But beyond the extension of full expensing, the interventions announced offered little to counter the impact of elevated interest rates on new project starts.

“If contractors are to find fertile ground for growth in 2024, it will be in decarbonisation projects which remain a priority for local authorities and investors alike.”

James Bailey, director and housing leader at PwC UK, said: “November’s PMI reading indicates the sustained impact from a challenging housing sales market, with an overall reading of 45.5 and house building in particular remaining a weak segment at 39.2. However, housebuilders are beginning to see grounds for cautious optimism. With mortgage rates beginning to show some signs of stabilising and many high street lenders beginning to cut rates to below 5%, there could be an uptick in buyer demand after the busy and typically expensive festive season.

“More broadly, we continue to see housebuilders increasingly exploring partnerships with private capital seeking rental products (affordable and private), although a continued period of price discovery and due diligence has prevailed over agreements and action to date. Looking forward, housing is shaping up to be a key battleground ahead of the General Election - the timing of which could be as early as Spring - and we expect the sector will become a more prominent focal point of manifestos with a range of supply and demand side commitments.”