Construction output continues decline as new orders crumble

The UK’s construction sector suffered another sharp reduction in construction output last month as political uncertainty and subdued client demand led to a downturn across all three broad categories of activity.

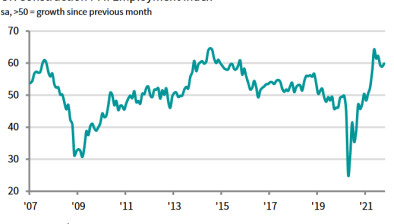

At 44.4 in December, down from 45.3 in November, the headline reading from the seasonally adjusted IHS Markit/CIPS UK Construction Total Activity Index registered below the crucial 50.0 no-change value for the eighth consecutive month. The current period of falling business activity across the construction sector is the longest recorded by the survey for almost a decade.

Civil engineering was by far the worst-performing category of construction in December, with activity falling at the fastest pace since March 2009. Anecdotal evidence suggested that political indecision and delays with contract awards for new projects had led to falling business activity.

Latest data also revealed a sharp drop in commercial work, which was partly attributed to clients opting to postpone spending decisions ahead of the general election. Meanwhile, house building dropped for the seventh month running in December, but the rate of decline was only modest.

Construction companies recorded a marked reduction in new business volumes during December, although the pace of contraction remained less severe than the ten-year record seen in August. The latest survey also pointed to the softest decline in staffing numbers for four months. Where a drop in employment levels was reported, survey respondents often cited the non-replacement of voluntary leavers amid a lack of work to replace completed projects.

A reduced pipeline of incoming new business led to falling demand for construction products and materials at the end of 2019. A robust and accelerated decline in input buying across the construction sector helped to alleviate some supply chain bottlenecks. As a result, vendor lead times lengthened to the least marked extent since September 2010.

Sluggish demand for construction inputs acted as a brake on pricing among suppliers in December. The latest increase in overall purchasing costs was only modest and the weakest recorded by the survey for almost ten years. Survey respondents noted that higher fuel and energy costs were the main drivers of rising input prices.

In contrast to the subdued output trends reported during December, construction companies indicated that their optimism towards the year-ahead business outlook rebounded to a nine-month high. A number of firms suggested that greater clarity in relation to Brexit had the potential to boost order books in 2020.

Tim Moore, economics associate director at IHS Markit, which compiles the survey, said: “December data suggested that the UK construction sector limped through the final quarter of 2019, with output falling in all three major categories of work. Brexit uncertainty and spending delays ahead of the General Election were once again the most commonly cited factors highlighted by firms experiencing a drop in construction activity.

“Civil engineering saw its sharpest decline for more than ten years and remained the worst-performing area of construction work, followed by commercial development. House building has been the most resilient category in recent months, but still declined overall during December.

“The forward-looking survey indicators provide some hope that the construction sector malaise will begin to recede in the coming months. Latest data indicated that the downturn in order books remains much less severe than the low point seen last August, which has already helped to bring employment numbers closer to stabilisation.

“Moreover, construction companies signalled that business optimism has recovered to its strongest for nine months. Survey respondents cited confidence that a more predictable domestic political landscape and clarity on Brexit could deliver a much-needed boost to clients’ willingness-to-spend in 2020.”

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, added: “The construction sector crumbled again in December under the weight of Brexit and political uncertainty as pipelines of work continued to worsen and new orders dropped for the ninth consecutive month.

“The civil engineering sector was the biggest victim of this new wave of decline registering its sharpest fall since March 2009. The relatively resilient residential sector also continued its downward spiral although at a slower rate compared to the last six months offering some small moderation in the face of reduced overall activity.

“As the General Election drew near, construction firms saw a spike in confidence believing indecision and political deadlock would shortly come to an end. However, the embedded frailties in the sector are laid out for all to see.

“Construction companies are still struggling to fill the skills gap left by the last recession and have had a bumpy ride since the referendum in 2016. It may take years to salvage the losses of the last three years, even if all obstacles are magically removed from the sector’s path to recovery. Whilst suppliers’ delivery times are on the verge of improving and input price inflation slowed to its lowest level since 2010, this will be cold comfort as the sector continues with one of its worst overall performances in the last ten years.”

Gareth Belsham, director of property consultancy and surveyors Naismiths, commented: “Despite the injection of confidence provided by the election result, it’s too early for any Lazarus-like rise in construction activity.

“December’s PMI survey revealed an industry still largely flat on its back. The fall in activity has yet to bottom out; eight straight months in negative territory is an unwanted honour not seen since the dark days of a decade ago.

“With even housebuilding activity – long the most resilient sector of the industry – falling, the sharp drops in both commercial and infrastructure construction could only drag the industry average one way.

“Yet for all that, December could still prove a turning point. The clear election result, and the prospect of an end to Britain’s Brexit deadlock, could unblock months and even years of repressed demand.

“Investor confidence is still brittle, so few expect the floodgates to open suddenly in 2020. While construction is an industry well used to peaks and troughs, the key question is how well it might respond if demand returns to more normal levels in the coming months.

“On that front there is some encouraging news in this largely grim set of data; the exodus of construction workers has slowed noticeably. The key thing is that contractors have enough capacity – i.e skilled people – on tap to handle an uptick in demand.

“On this evidence the capacity is there, even if new orders have yet to follow suit.”