Housing downturn leads sector slide, PMI finds

UK construction output fell at a faster pace in February as a deepening slump in housebuilding dragged the sector back into sharper contraction, according to the latest S&P Global UK Construction PMI.

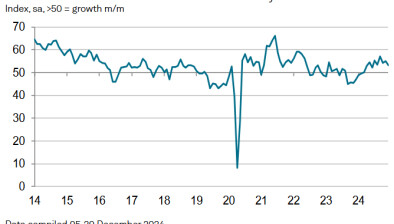

The headline PMI dropped to 44.5, down from 46.4 in January, signalling a solid and accelerated decline in overall activity. Firms pointed to weak order books, a lack of new project starts and, in many cases, exceptionally wet weather that disrupted work on site.

Residential building remained the worst‑performing category, with an index reading of 37.0 and a quicker rate of decline than in January. Commercial activity also fell more sharply (46.5), though the downturn was less severe than in other parts of the industry.

Civil engineering was the only segment to see a slower contraction, with an index of 41.0, the mildest decline since September 2025.

New work across the sector fell steeply for the 14th consecutive month. While demand remained subdued, some firms reported an uptick in tender opportunities for infrastructure and energy projects, hinting at potential future stabilisation.

Despite the downturn, business sentiment strengthened to its highest level since December 2024. Around 42% of firms expect activity to rise over the next year, compared with just 12% anticipating a fall. Expectations were supported by hopes of major project wins and a broader economic recovery later in 2026, though political and economic uncertainty continues to weigh on decision‑making.

Employment levels were close to stabilising in February, marking a notable improvement from the sharp job losses recorded at the end of 2025.

Purchasing activity continued to decline sharply, helping suppliers improve delivery times for the seventh month running. However, firms faced renewed pressure on margins as input costs rose at their steepest rate since July 2025, driven by higher prices for concrete, copper, insulation and steel.

Tim Moore, economics director at S&P Global Market Intelligence, said the sharper fall in housebuilding was the “main factor” behind February’s setback.

“Total industry activity has decreased in each month since January 2025 and the latest decline was faster than seen on average over this period,” he said. “Construction companies were hopeful of a turnaround… linked to forthcoming new projects in the infrastructure and energy sectors.”

Brian Smith, head of cost management at AECOM, said firms would be disappointed not to see a third month of improvement but argued the downturn may be close to bottoming out.

“Pipelines remain strong and we’ll see much of the planned work start to land on site in the coming months,” he said. “But firms can’t let complacency creep in… contractors that maintain strong margins will be those leveraging AI and digital tools to maximise efficiency.”

Atul Kariya, head of real estate and construction at MHA, warned that the sector remains vulnerable to external shocks.

“Global instability and ongoing conflicts will put further pressure on supply chains and exacerbate energy and materials cost inflation,” he said. “The industry urgently needs clear, sustained measures that stimulate economic activity and support investment.”

Kariya added that unemployment trends could weigh on housing demand in the months ahead, but said gradual stabilisation was still possible if the right policy environment emerges.