UK construction sector sees sharpest decline since early pandemic

The UK construction industry endured its steepest contraction in more than five years during November, as weak client confidence and delayed spending decisions ahead of the Budget weighed heavily on activity.

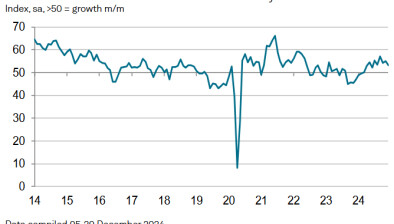

The headline S&P Global UK Construction Purchasing Managers’ Index (PMI) dropped to 39.4 in November, down from 44.1 in October, marking the lowest reading since May 2020. Output volumes have now fallen for eleven consecutive months.

Sub-sector data revealed widespread weakness:

- Housing activity fell to 35.4

- Commercial construction dropped to 43.8

- Civil engineering slumped to 30.0

All three categories recorded their fastest downturns in five-and-a-half years, with survey respondents citing fragile market confidence, delayed project releases, and a lack of new work.

Around 44% of firms reported a fall in new orders, compared with just 17% signalling an increase. Excluding the pandemic period, this represented the sharpest decline in new work since early 2009.

Employment also fell for the eleventh month in a row, with November’s job losses the steepest since August 2020. Subcontractor usage continued its downward trend, while buying activity dropped at the fastest pace in over five years.

There were some positives: supplier performance improved solidly, the best since June 2024, as softer demand alleviated supply chain pressures. However, input costs rose at an accelerated pace, particularly for electrical components, copper products, and insulation, though inflation remained below the long-run survey average.

Tim Moore, economics director at S&P Global Market Intelligence, said the data showed “a sharp retrenchment across the UK construction sector,” with infrastructure and residential building leading the downturn. He noted that optimism for the year ahead had fallen to its lowest since December 2022.

Jordan Smith, regional director at Thomas & Adamson, described the PMI as “a stark picture,” highlighting fragile client confidence and delayed spending decisions. He pointed to improving supply chains and more manageable inflation as potential stabilisers heading into 2026.

Brian Smith, head of cost management at AECOM, welcomed government commitments to capital spending and planning reform but warned that “clients need to see further progress before committing to new projects.” He emphasised the role of AI and digital tools in speeding up planning reviews.

Atul Kariya, head of real estate and construction at MHA, stressed that despite Budget measures, “the underlying reality remains the same: rising labour costs, ongoing planning delays, global headwinds and the potential dampening effect of a mansion tax are still weighing heavily on sentiment.” He added that long-term stability and predictability in policy are essential for investment.

Looking ahead, 31% of firms expect an upturn in activity over the next 12 months, narrowly outweighing the 25% forecasting a decline. Yet the Future Activity Index signalled the weakest optimism since late 2022.

While targeted public-sector investment and lower borrowing costs could provide support, the sector faces persistent structural pressures—from wage growth and compliance costs to housing market uncertainty. As Kariya noted, “The sector has shown its resilience time and again, but it can only convert that resilience into growth when operating in a stable environment.”